The Comparison at a Glance

Before we dive into each option, here’s a quick snapshot of how they compare across the factors that matter most to NRIs:

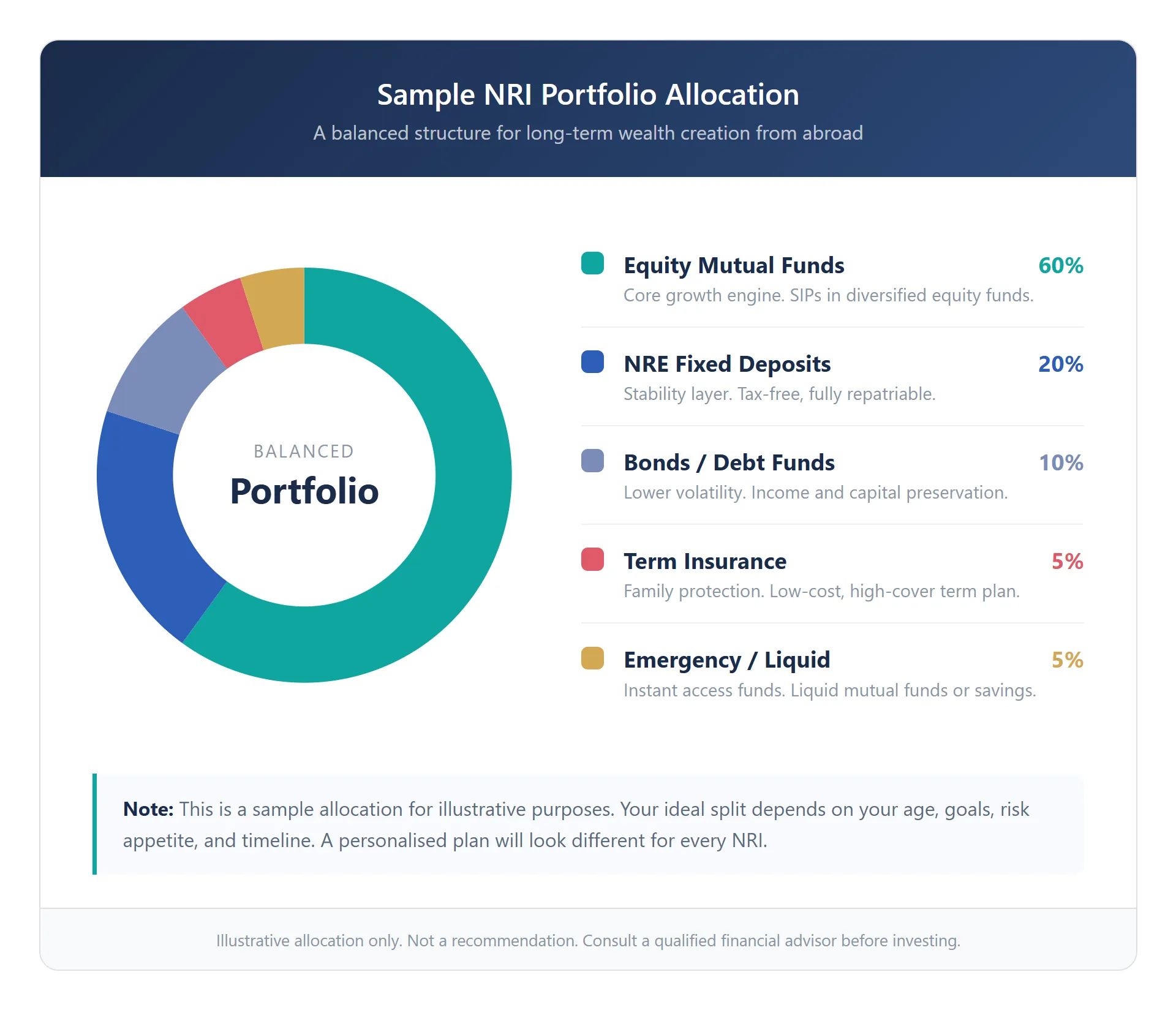

Mutual Funds (Equity): Historical returns of 11–14% CAGR over 10-year periods. Long-term gains taxed at 12.5% above ₹1.25 lakh. Start from ₹500/month via SIP. Fully liquid (redeem anytime, money in 2–3 days). Fully manageable from abroad — set up once and automate.

NRE Fixed Deposits: Returns of 6.50–7.50% per annum. Interest is completely tax-free in India. Minimum typically ₹10,000. Locked for the tenure (1–10 years), but premature withdrawal is possible with a penalty. Zero ongoing management.

Direct Equity (Stocks): Potential returns of 12–18%+ but highly variable. Same tax treatment as equity mutual funds. Requires a PIS account, demat account, and active monitoring. Difficult to manage consistently from abroad.

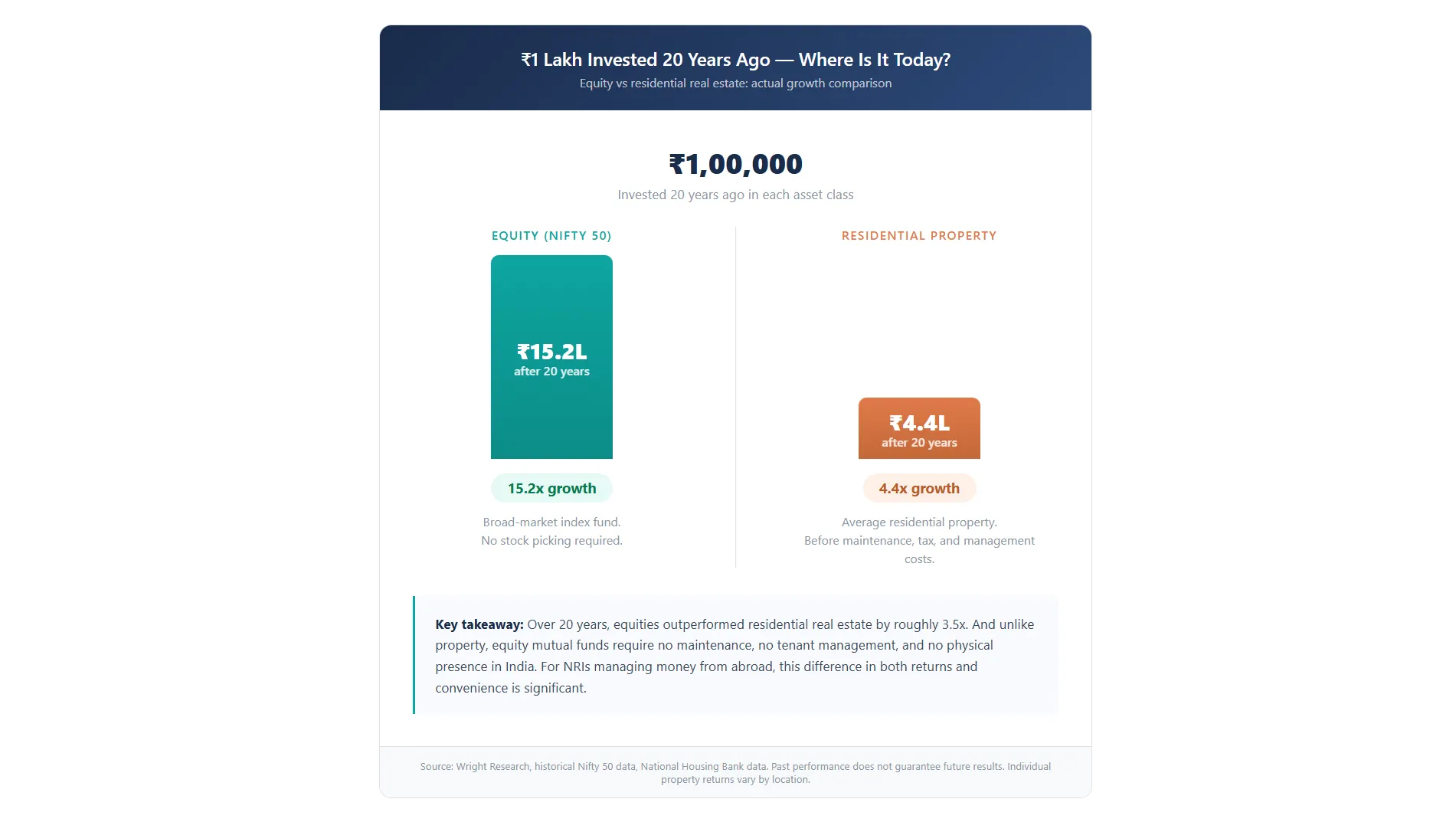

Real Estate: Capital appreciation historically 6–10% in metro areas, but net rental yields just 2–3% after expenses. Long-term capital gains taxed at 12.5%. Requires very large capital (₹30 lakh–₹2 crore+ depending on city). Extremely illiquid — selling takes months. Ongoing management is a significant challenge from abroad.

Bonds and Debt Instruments: Returns of 7–9% depending on type and tenure. Tax at your income slab rate for most debt instruments. Lower risk, lower volatility. Limited ongoing involvement.

Term Life Insurance: Not an investment — no returns. It’s pure protection. But it belongs in every NRI’s financial plan before anything else.

Mutual Funds — The Core of Most NRI Portfolios

There’s a reason mutual funds consistently come out on top for NRIs, and it’s not just about returns.

On the tax side, equity mutual funds (held over 12 months) attract long-term capital gains tax at 12.5% only on gains exceeding ₹1.25 lakh per year. That’s one of the most efficient tax treatments across all NRI investment options. “NRI mutual fund taxation in detail“

The catch: With thousands of funds available, choosing the right ones — and structuring them into a portfolio that actually works together — is where most NRIs get stuck. That’s exactly what we help with. We build portfolios tailored to your goals, your time horizon, and your tax situation, so you’re not guessing or picking funds based on last year’s rankings.

NRE Fixed Deposits — The Safe, Tax-Free Foundation

Where they fall short: After inflation (which runs 4–6% in India), your real returns are modest — sometimes barely positive. FDs protect your money, but they don’t grow it. If your entire India portfolio is in fixed deposits, you’re almost certainly losing purchasing power over the long term.

The smart approach — and what we typically recommend — is to use NRE FDs for your emergency fund in India and for money you’ll need within 1–3 years, while allocating the growth portion of your portfolio to equity mutual funds. Getting that balance right depends on your specific situation, and it’s something we help NRIs with every day. and what we typically recommend — is to use NRE FDs for your emergency fund in India and for money you’ll need within 1–3 years, while allocating the growth portion of your portfolio to equity mutual funds. Getting that balance right depends on your specific situation, and it’s something we help NRIs with every day.

Direct Equity — Higher Potential, Higher Demands

NRIs can invest in Indian listed stocks through delivery-based trades (intraday trading isn’t permitted under FEMA). You’ll need a PIS account through a designated bank, a demat account, and a trading account. Budget 2026 doubled the individual NRI cap in any single company from 5% to 10%.

The reality we see: Most NRIs who start with direct equity eventually find it difficult to manage consistently from abroad. Positions become reactive rather than strategic. This is why equity mutual funds — where professionals manage the stock selection — tend to be a better fit for the majority of NRIs. If you’re experienced and enjoy it, stocks can play a role. But for most people, mutual funds deliver comparable long-term equity exposure with far less effort.

Real Estate — The Emotional Favourite That Often Disappoints

Then there’s the practical reality of managing property from abroad: finding reliable tenants, handling maintenance, dealing with legal paperwork, and navigating the selling process (which involves heavy TDS compliance for NRIs). “NRI real estate guide“

Our take: Real estate can have a place in your overall wealth picture, but it shouldn’t be the core. If you want property exposure without the management headache, REITs (Real Estate Investment Trusts) offer 7–10% yields, trade on the stock exchange, and require no property management whatsoever. We can help you evaluate whether direct property or REITs make more sense for your situation.

Bonds and Debt Instruments — The Stability Layer

Where they fit: Bonds and debt funds work as a supporting allocation — typically 15–25% of a portfolio — to reduce overall volatility. They’re not a growth engine on their own. We factor these in when building balanced portfolios for NRIs who want stability alongside equity growth.

Term Insurance — The One Thing That Should Come Before Any Investment

The critical mistake we see: NRIs buying endowment plans or ULIPs marketed as “investment-cum-insurance.” These products typically deliver 4–6% returns — worse than a basic NRE FD — while locking your money for 15–20 years. Keep insurance and investment completely separate. “term insurance for NRIs“

We help NRIs select the right term plan based on your coverage needs, family situation, and country of residence. It’s one of the first things we recommend getting in place.

So Which Option Is Best? The Honest Answer

Frequently Asked Questions

Which NRI investment gives the highest returns?

Are NRE fixed deposits better than mutual funds?

Should NRIs invest in real estate or mutual funds?

What is the most tax-efficient investment for NRIs?

How much should NRIs allocate to each investment type?

Let Us Build the Right Structure for You

Disclaimer: This article is for informational purposes only and does not constitute financial, tax, or legal advice. Tax laws and FEMA regulations are subject to change. Mutual fund investments are subject to market risks — please read all scheme-related documents carefully. Consult a SEBI-registered investment advisor and a qualified tax professional before making investment decisions.