For NRIs building wealth in India, this is one of the most common questions our team gets asked — and one of the most misunderstood.

The standard advice on the internet tells you fixed deposits are safe but slow, and mutual funds are higher risk but higher return. That’s broadly true. But it misses the most important part of this conversation for NRIs specifically: the NRE fixed deposit is one of the most tax-efficient savings instruments available anywhere in the world. That changes the comparison significantly — and it means the answer to “which is better?” is more nuanced than most people realise.

Here’s the full, honest picture.

Why This Comparison Is Different for NRIs

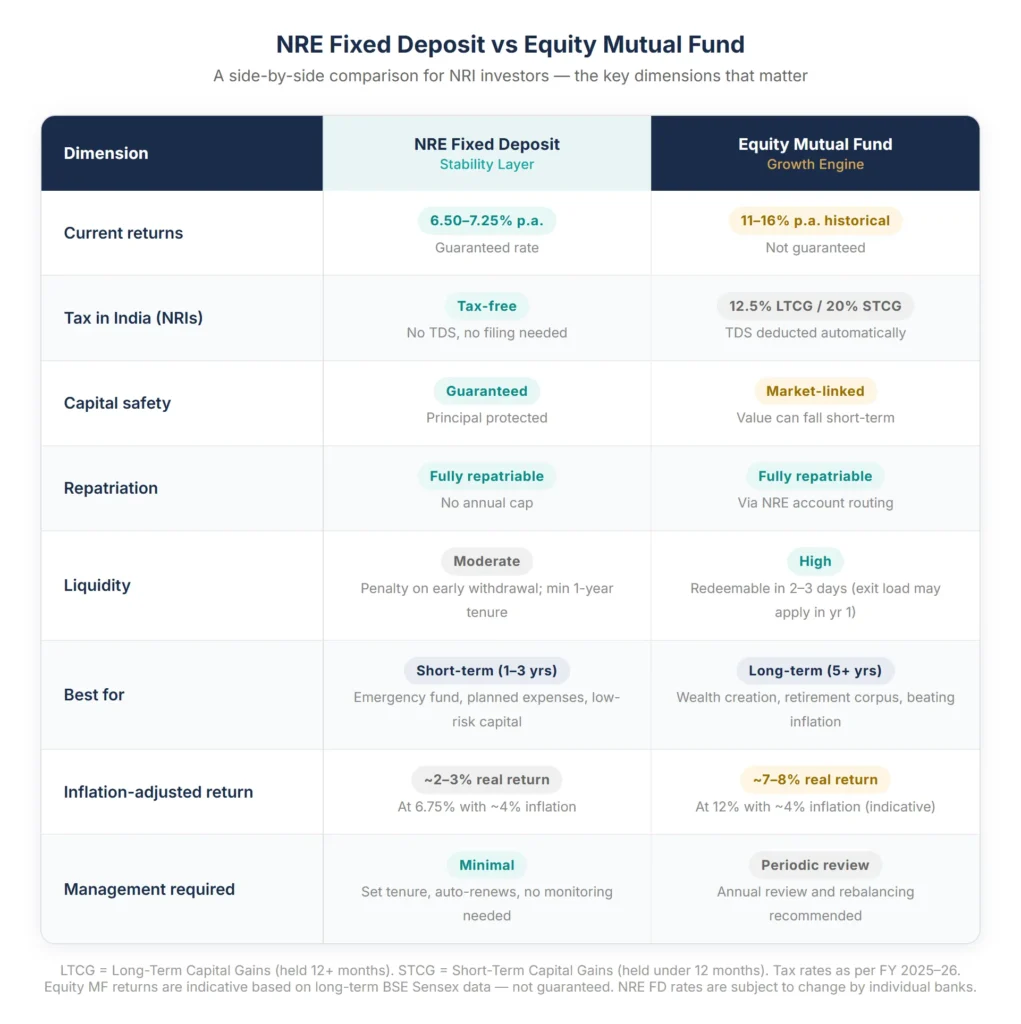

A resident Indian investing in a fixed deposit pays income tax on the interest at their applicable slab rate — which can be as high as 30%. For them, a 7% FD is really a 4.9% return after tax.

An NRI investing through an NRE fixed deposit pays zero tax on the interest in India. The full 6.50–7.25% that top banks are currently offering goes directly into their pocket, with no deduction at source and no filing required to claim it back. And both the principal and the interest are fully repatriable — you can move the money back to your country of residence without any cap or annual limit.

This is a meaningful advantage. But it’s only part of the story.

For a complete picture of “how NRE accounts work and how to set one up” , we’ve covered that separately. What this blog focuses on is the investment decision: given everything NRE FDs offer, when does it still make sense to invest in equity mutual funds instead — and why?

What NRE Fixed Deposits Actually Offer in 2026

Current NRE FD rates across major Indian banks sit in the range of 6.50% to 7.25% per annum for tenures of one year and above. The key features:

- Tax-free interest in India — exempted under the Income Tax Act. No TDS, no need to claim a refund.

- Fully repatriable — principal and interest can be moved abroad freely, with no annual cap.

- Capital guaranteed — deposits up to ₹5 lakh are insured under DICGC; the principal is not subject to market movement.

- Premature withdrawal — possible, but attracts a penalty. Rates are typically reduced by 0.5–1% for early closure, and no interest is paid if withdrawn before one year.

- Minimum tenure — most banks require a minimum of one year for NRE FDs.

For NRIs, this is genuinely a strong product. A 6.75% tax-free return (using the midpoint of the current range) is higher than what most developed-country savings accounts, government bonds, or fixed-income products offer — and you’re getting it with full repatriation flexibility.

The question is: is 6.75% enough for where you want your wealth to be in 10, 15, or 20 years?

What Equity Mutual Funds Offer Over the Long Term

Indian equity mutual funds — invested in companies listed on the BSE and NSE — have delivered annualised returns of 9.5% to 15.9% over 10 to 20-year periods based on BSE Sensex data. The 10-year annualised return sits at approximately 15.9%, the 15-year at 9.5%, and the 20-year at 11.2%.

These returns are not guaranteed. Equity markets move up and down, sometimes significantly. An NRI investing in equity mutual funds should expect periods where the value of their portfolio falls — sometimes by 20–30% in a bad year — before recovering over the medium term.

But here’s what makes equity mutual funds powerful for long-term NRI wealth creation:

- Compounding at higher rates — the gap between 7% and 12% looks small annually but becomes enormous over 15–20 years (we show the numbers below)

- Inflation-beating returns — India’s CPI inflation has averaged around 4–5% historically, and currently sits at 3.40% (March 2026). An FD at 6.75% delivers a real return of roughly 2–3% after inflation. Equity at 12% delivers a real return of 7–8% — a fundamentally different outcome for long-term purchasing power

- Liquidity — unlike FDs with lock-in periods and premature withdrawal penalties, equity mutual funds can typically be redeemed within 2–3 business days, without penalty (subject to exit loads in the first year for some funds)

If you’re unsure which balance of FDs and mutual funds makes sense for your situation, this is exactly the kind of question our team works through with NRI clients. Reach out and we’ll help you think it through.

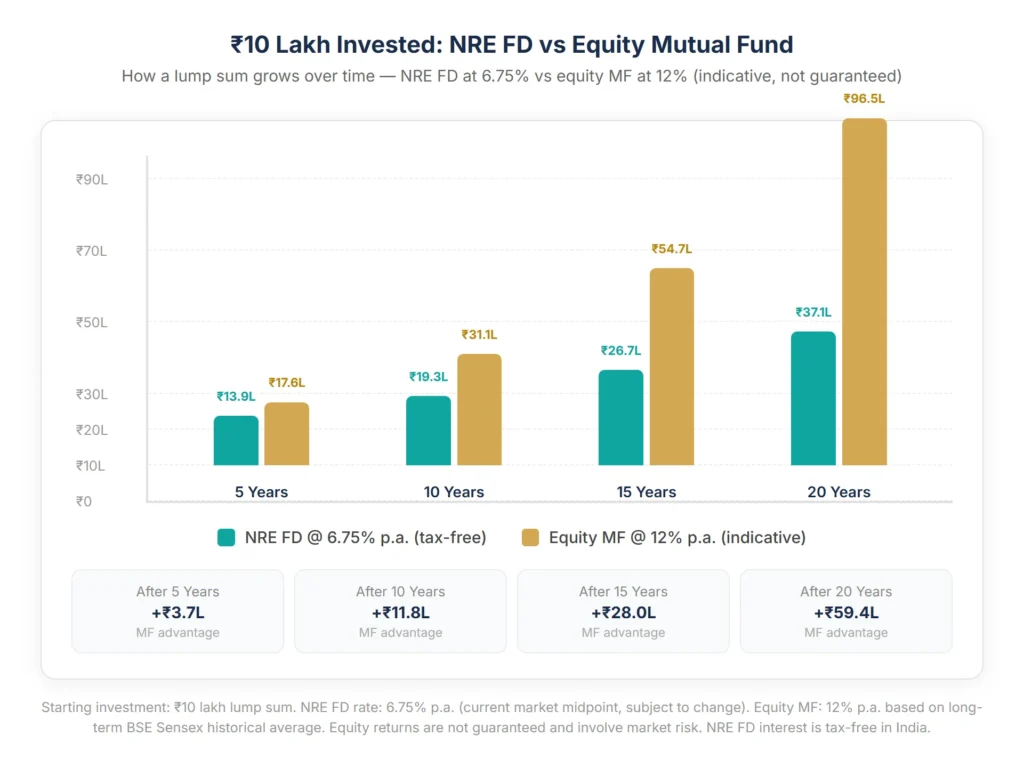

The Number That Changes Everything: Growth Over Time

Here’s what ₹10 lakh invested as a lump sum looks like under both options over time, assuming 6.75% for the NRE FD (current midpoint) and 12% for equity mutual funds (conservative long-term assumption based on historical Sensex data):

The visual alongside this blog shows this growth comparison graphically — the lines look similar in year 5, begin to diverge noticeably by year 10, and by year 20 the gap has become almost unrecognisable.

This is what compounding at different rates does over long time horizons. The FD doesn’t fail you — it grows your money steadily and safely. But at 6.75%, it cannot keep pace with equity over 15–20 years.

Important: The 12% assumption for equity is based on long-term historical BSE Sensex performance. It is indicative, not guaranteed. Actual returns will vary, and equity carries the risk of loss. Mutual fund investments are subject to market risks.

When Fixed Deposits Are the Right Choice for NRIs

There are clear situations where an NRE FD is not just acceptable — it’s the right tool:

Short-term goals (1–3 years). If you need the money within three years — for a property purchase, a family event, or a planned return to India — equity mutual funds are too volatile. A market correction in year two could leave you with less than you started. An FD at 6.75% gives you certainty of outcome.

Emergency fund. Every NRI with financial commitments in India should have 3–6 months of India-side expenses parked in an NRE savings account or short-term FD. This is capital you need to access quickly and without loss — not suitable for equity.

Capital you cannot afford to lose. If the money you’re considering investing represents a significant portion of your net worth and you have low tolerance for volatility, the guaranteed return of an FD may serve you better than the higher but uncertain returns of equity.

Repatriation-priority capital. Because NRE FDs are fully repatriable with no annual cap, they’re particularly useful for money you know you’ll want to move back abroad within a defined timeframe. Mutual fund redemptions are liquid but still require coordination — an FD with a known maturity date can be planned around repatriation needs precisely.

When Mutual Funds Are the Right Choice for NRIs

Wealth creation over 5+ years. For money you won’t need for at least five years — and ideally ten or more — equity mutual funds have historically been the superior wealth-creation tool in India. The compounding numbers above make this clear.

Beating inflation meaningfully. A 6.75% NRE FD currently delivers a real return (after inflation) of approximately 2–3%. That preserves purchasing power, but it doesn’t grow it significantly. For NRIs building a retirement corpus or children’s education fund, a 2–3% real return over 20 years may leave them short of where they need to be.

Regular monthly investing. If you want to invest consistently from your overseas income each month, a “systematic investment plan (SIP)” in an equity mutual fund is designed exactly for this — automated, disciplined, and requiring no active management between reviews.

Portfolio growth, not just preservation. For NRIs in their 30s and 40s with a long runway ahead of them, the primary job of a large portion of their India portfolio is growth — not safety. Equity mutual funds are built for that job.

Many of our NRI clients initially had the majority of their India savings in FDs — comfortable and familiar. After reviewing the long-term numbers together, most chose to gradually shift a portion toward equity. If you’d like to do a similar review of your current setup, our team is happy to help. There’s no obligation — just a clear picture of what your money is currently doing and what it could be doing.

The Answer Most NRIs Actually Need: Both, in the Right Proportion

The right answer for most NRIs isn’t “FD or mutual fund.” It’s “FD and mutual fund — for different purposes.”

A well-structured India portfolio typically looks something like this:

- Stability layer (NRE FDs, 20–30% of India allocation): Emergency fund, short-term goals, capital you’ll need within three years. Fully liquid and repatriable. Earns tax-free at 6.5–7.25%.

- Growth engine (Equity mutual funds, 60–70% of India allocation): Long-term wealth creation. 10+ year horizon. Compounding at historically 11–16% over market cycles. Accepts short-term volatility in exchange for long-term outperformance.

- Transition layer (Hybrid or debt funds, 10–20%): For goals 3–5 years away. Lower volatility than pure equity, higher return potential than FDs.

What most NRIs discover, when they look at the long-term numbers honestly, is that the FD isn’t the problem — the over-reliance on FDs at the expense of equity is. Both instruments deserve a place. The question is how much of each, and for what purpose.

If you’d like our team to map out the right balance for your specific situation — your timeline, your goals, your current holdings — reach out for a conversation. We work through exactly this with NRI clients regularly, and it usually takes one clear conversation to turn a scattered collection of FDs and random investments into a portfolio that actually makes sense.

Frequently Asked Questions

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Past performance is not indicative of future results. The return assumptions used in this blog (12% for equity mutual funds, 6.75% for NRE FDs) are based on historical averages and current market rates respectively — they are not guaranteed. Fixed deposit interest rates are subject to change at the discretion of individual banks. Tax rules and FEMA regulations are subject to change; always verify the latest position with a qualified advisor. This blog is for general informational and educational purposes only and does not constitute personalised financial advice. NRIs should consult a qualified financial advisor and tax professional for guidance specific to their country of residence and individual circumstances. We specialise in Indian financial products and Indian tax laws only.