Here’s a scenario that trips up thousands of NRIs every year.

You earn a salary in the UK, Australia, or the UAE. You also have rental income, fixed deposit interest, or mutual fund gains flowing in from India. Come tax season, India deducts TDS at source. Then your country of residence wants its cut too.

Two countries. One income. Two tax bills.

This is exactly what the Double Taxation Avoidance Agreement — commonly called DTAA — was designed to prevent. And if you’re an NRI with any income from India, understanding DTAA isn’t optional. It’s one of the most powerful tools available to you, and most NRIs either don’t know it exists or don’t know how to use it properly.

Let’s change that.

What Is DTAA, in Plain English?

DTAA is a tax treaty signed between two countries that decides: when the same income could be taxed in both places, which country gets to tax it — and at what rate.

India has signed comprehensive DTAAs with over 90 countries, including the UK, USA, UAE, Australia, Canada, Singapore, Germany, and most of the Gulf nations. The full and current list is maintained by the Income Tax Department of India.

The core principle is simple: you should not pay full tax on the same rupee twice. DTAA either eliminates the double tax entirely, or reduces one country’s tax rate so the combined burden is fair.

Why This Matters for You as an NRI

Without DTAA, here’s what India would automatically deduct from your India-sourced income:

- NRO fixed deposit interest: 30% TDS (plus applicable surcharge and cess)

- Rental income: 30% TDS

- Mutual fund gains: 20% on short-term gains, 12.5% on long-term gains (for equity funds)

- Dividends: 20% TDS

Then, depending on where you live, your country of residence may also treat that same income as taxable — because it came from overseas.

DTAA steps in and prevents this pile-up. Depending on the treaty your country has with India, the TDS rate can be reduced significantly, or the income may be exempt from tax in one country altogether.

Wondering how DTAA connects to your investment strategy? Our team helps NRIs set up the right documentation before investing so you’re not leaving money on the table at tax time.

How DTAA Actually Works: Four Country Scenarios

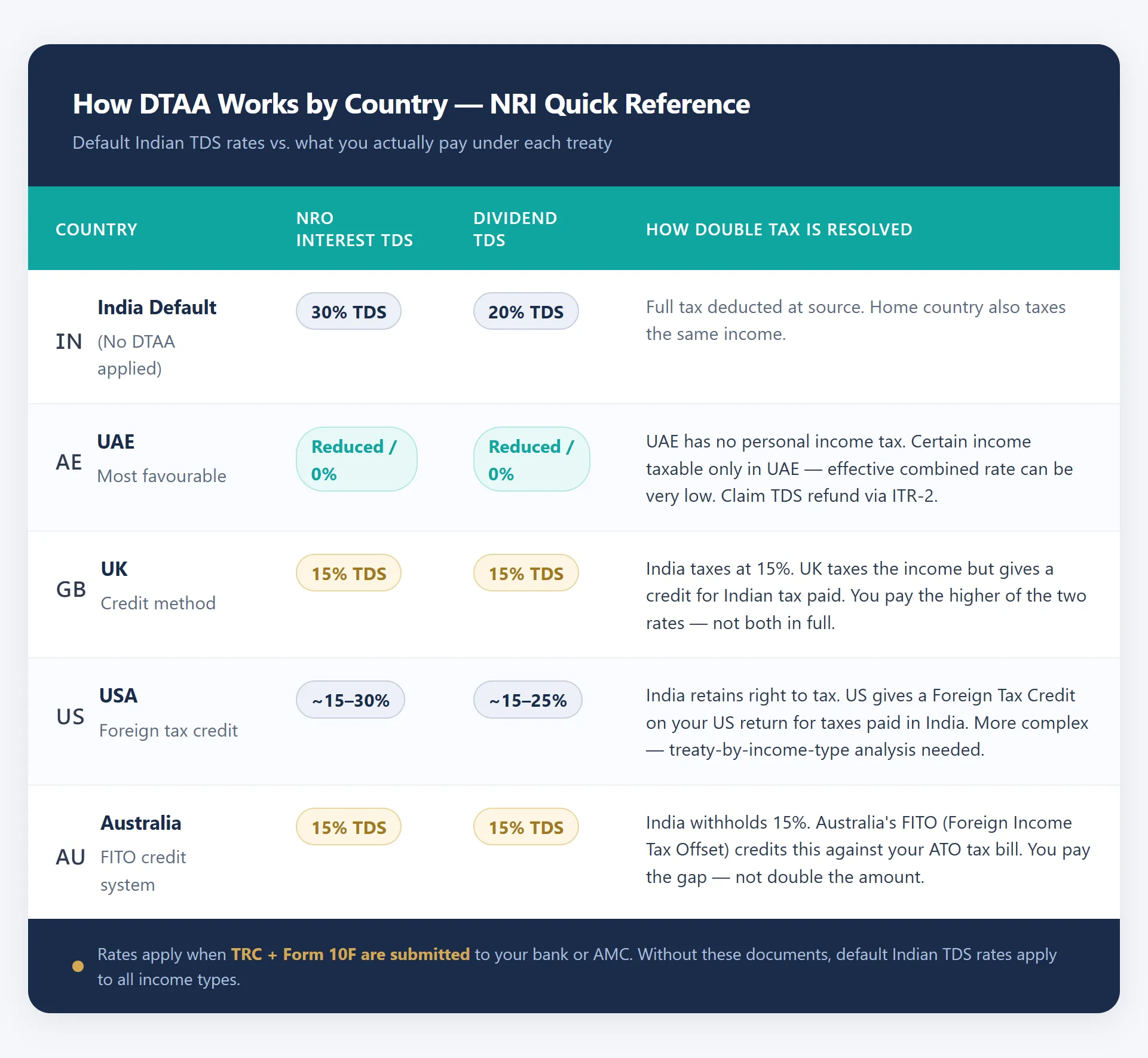

Scenario 1: You Live in the UAE

The India–UAE DTAA is one of the most favourable for NRIs. Interest income on NRO deposits and certain investment income is taxable only in the UAE — and the UAE currently levies no personal income tax.

In practice: India may still deduct TDS at source (because the bank doesn’t know you’ve filed Form 10F), but you can claim a refund when you file your Indian income tax return.

Scenario 2: You Live in the UK

Under the India–UK DTAA, dividend income is taxed at a reduced rate of 15% in India (instead of the default 20% TDS). Interest income is taxed at 15% rather than 30%. You can then claim a credit for the Indian tax paid when filing in the UK, so you’re not double-taxed — you’re taxed once at the higher of the two rates.

Scenario 3: You Live in the USA

The India–US DTAA is more complex. It does not eliminate Indian taxation on most types of income — instead, it allows US NRIs to take a foreign tax credit on their US return for the taxes they’ve already paid in India. The result: you’re taxed at the higher rate overall, but not twice over.

Scenario 4: You Live in Australia

Under the India–Australia DTAA, interest income from NRO deposits is capped at 15% TDS in India (down from the default 30%). Dividends are also taxed at a maximum of 15% in India. Australia then applies its Foreign Income Tax Offset (FITO) system — meaning the Indian tax you’ve already paid is credited against your Australian tax bill. So if India withheld 15% and your Australian marginal rate is 32.5%, you pay the 17.5% difference in Australia — not both in full. The same income is taxed once, at your highest applicable rate across both countries combined.

This is exactly why the country you live in changes your strategy significantly. The rules aren’t the same across the board — which is why cookie-cutter advice doesn’t work for NRIs.

The Two Documents That Unlock DTAA Benefits

DTAA relief doesn’t happen automatically. You need to prove your tax residency to claim it. There are two documents required:

1. Tax Residency Certificate (TRC)

This is a certificate issued by the tax authority of your country of residence, confirming that you are a tax resident there. In the UK, this comes from HMRC. In the UAE, from the Federal Tax Authority. In Australia, from the ATO.

2. Form 10F

This is a self-declaration form filed with the Indian Income Tax Department. It contains your basic details (PAN, address, tax identification number from your country of residence) and confirms you’re relying on the DTAA. Since 2023, Form 10F must be filed online through India’s e-filing portal for most NRIs.

Together, these two documents allow the AMC, bank, or payer to either apply a reduced TDS rate at source — or allow you to claim a refund of excess TDS when filing your ITR-2.

What Income DTAA Covers — and What It Doesn't

DTAA applies to most types of passive India-sourced income:

- Interest income (NRO FDs, bonds)

- Dividend income (stocks, mutual fund dividends)

- Capital gains (property sales, mutual fund redemptions — though the treatment varies by treaty)

- Rental income

- Royalties and professional fees (for those with India-based business income)

Important nuance on capital gains: Not every DTAA gives India the right to exempt or reduce tax on capital gains. Some treaties (like India–Mauritius and India–Singapore) had special capital gains clauses that have since been amended. Under the current framework, equity and mutual fund gains are generally taxable in India regardless of DTAA, though some treaties still offer relief — which is why getting advice specific to your country matters.

Not sure which DTAA provisions apply to your country? This is the kind of detail our team handles as part of the investment setup process — so your tax documents are in place before your first SIP goes in.

NRE vs NRO: How Your Account Choice Affects DTAA Relevance

Here’s a nuance many NRIs miss: DTAA is primarily relevant to NRO account income, not NRE account income.

Why? Because interest earned on an NRE account is fully exempt from Indian tax under the Income Tax Act itself — no DTAA required. NRE FD interest is tax-free in India, end of story.

NRO account income — earned from Indian salary, rent, pension, or domestic fixed deposits — is taxable in India. This is where DTAA becomes essential to prevent your home country from taxing it a second time.

Choosing the wrong account for the wrong purpose doesn’t just create compliance headaches — it can mean paying tax you were never legally required to pay.

A Common Mistake: Assuming DTAA Means Zero Tax

DTAA does not automatically mean zero Indian tax. It means reduced or eliminated double tax. In most cases, India still retains the right to tax income arising in India — DTAA just ensures your home country gives you credit for what India has already taken.

The exception is for countries like the UAE where personal income tax doesn’t exist. In that case, you benefit from lower or zero TDS on certain income types in India — and pay nothing at home.

Understanding this distinction saves a lot of confusion when NRIs open their first tax refund statement and see TDS was deducted despite being UAE-based.

What to Do Right Now

If you have any income from India — rental, FD interest, dividends, or mutual fund gains — here’s the practical action list:

- Confirm your country has a DTAA with India (it almost certainly does if you’re in the UK, UAE, USA, Australia, Canada, Singapore, or the Gulf)

- Obtain your Tax Residency Certificate from your local tax authority

- File Form 10F on India’s income tax e-portal: File Form 10F online

- Provide both documents to your bank, AMC, or fund manager before income is generated — not after

- File your Indian ITR-2 to claim any TDS refunds due

The earlier these are in place, the less you’ll pay unnecessarily.

Getting DTAA documentation right is one of the first things we sort for every NRI client. It’s not complicated when you have someone who knows the process — it just needs to be done before the income starts flowing.

Frequently Asked Questions About DTAA for NRIs

Disclaimer: This blog is for general informational purposes only and does not constitute financial, tax, or legal advice. Tax laws, DTAA provisions, and TDS rates are subject to change. The DTAA treatment of your India-sourced income depends on your specific country of residence, the nature of the income, and individual circumstances. Always consult a qualified tax advisor who specialises in cross-border taxation before making investment or tax decisions. Mutual fund investments are subject to market risks — please read all scheme-related documents carefully before investing.