Mutual fund taxation in India changed meaningfully after the July 2024 Union Budget, and those changes are fully in effect as of 2026. If you’re an NRI investing in Indian mutual funds — or considering it — the tax picture today looks quite different from what it did even two years ago.

This blog gives you the complete, current framework: what you actually pay on equity, debt, and hybrid mutual fund returns as an NRI, how TDS works, what makes NRI taxation different from resident investors, and what you need to do to avoid paying more tax than you owe.

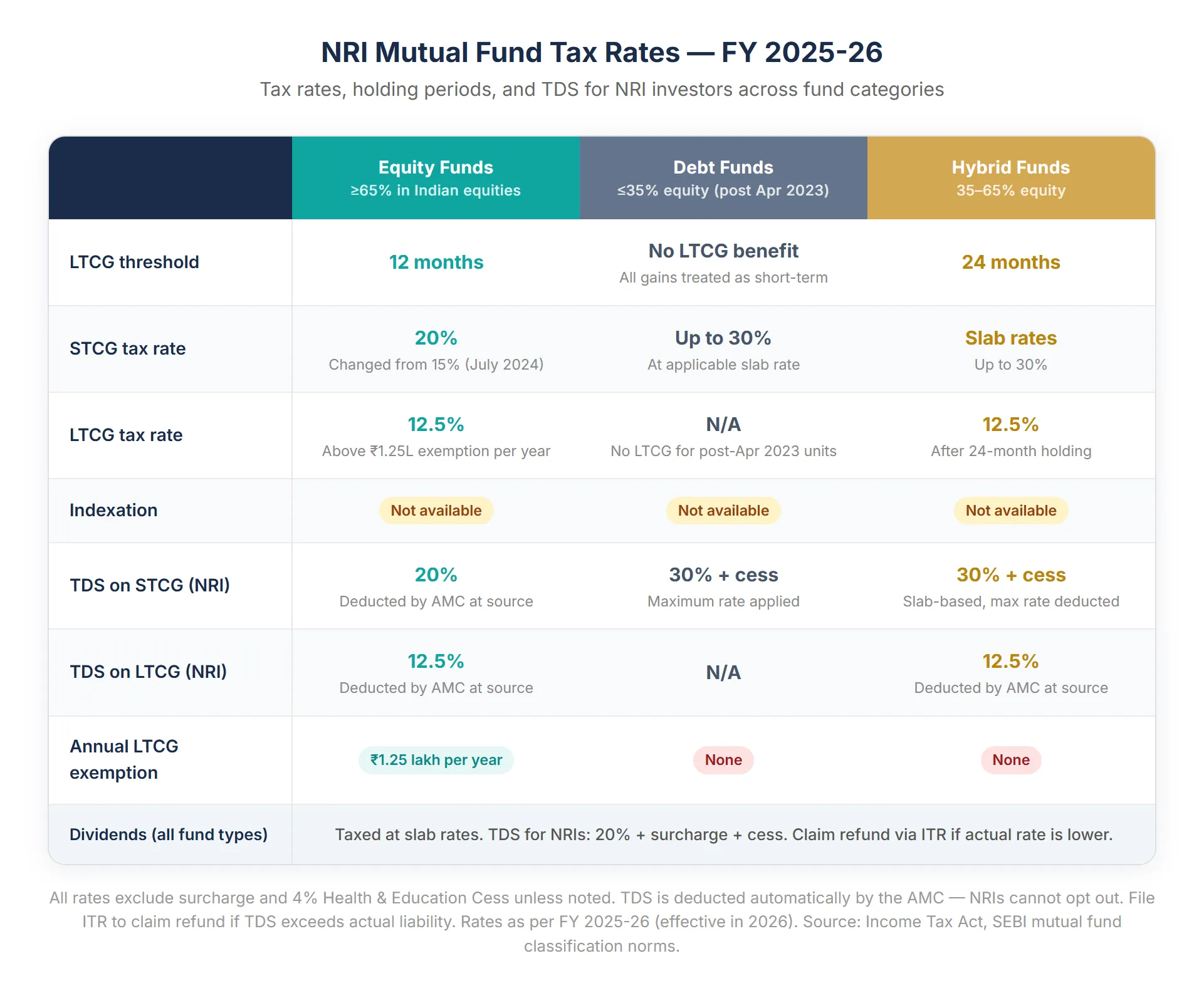

All rates and rules in this blog reflect the position as of FY 2025-26 — the tax year in effect right now.

The Two Things That Determine Your Tax

Every mutual fund tax calculation in India comes down to two variables:

1. What type of fund is it? SEBI classifies funds by their equity exposure. Funds with 65% or more in Indian equities are “equity-oriented.” Funds below 35% in equity fall into the debt category. Funds between 35% and 65% are hybrid. The classification determines which tax rules apply.

2. How long did you hold it? The holding period — measured from the date you bought the units to the date you sold them — determines whether your gain is short-term (STCG) or long-term (LTCG). Each category has a different holding threshold.

Equity Mutual Funds: The Tax You Pay as an NRI

Equity-oriented mutual funds include large cap, mid cap, flexi cap, index funds, ELSS, and aggressive hybrid funds — any scheme where 65% or more of the portfolio is invested in Indian equities.

Holding period threshold: 12 months.

Short-term capital gains (held under 12 months): Taxed at 20%. This rate increased from 15% in the July 2024 Budget and applies to all transfers from 23 July 2024 onwards.

Long-term capital gains (held 12 months or more): Taxed at 12.5% on gains exceeding ₹1.25 lakh per financial year. The first ₹1.25 lakh of equity LTCG in any given year is exempt. This exemption threshold was increased from ₹1 lakh, and the rate from 10%, in the same July 2024 Budget.

No indexation benefit applies to equity LTCG. The 12.5% rate is applied to the nominal gain — purchase price subtracted from sale price, without any inflation adjustment.

How TDS works for NRIs: When you redeem equity mutual fund units, the AMC (fund house) automatically deducts TDS before crediting your proceeds. For equity funds, TDS is deducted at 12.5% on LTCG and 20% on STCG. You don’t have a choice about this — it happens at source. If the TDS deducted exceeds your actual tax liability (for example, if your LTCG is below the ₹1.25 lakh exemption), you can claim a refund by filing an ITR.

Debt Mutual Funds: A Different Tax Picture Entirely

Debt-oriented mutual funds — including liquid funds, ultra short duration, money market, corporate bond, gilt, and banking & PSU funds — follow different rules that changed significantly from April 2023.

For units purchased after 1 April 2023: All gains are treated as short-term regardless of how long you hold them. There is no LTCG benefit, no special rate, and no indexation. The gains are added to your income and taxed at your applicable slab rate — which for most NRIs with meaningful Indian income means up to 30% plus surcharge and 4% cess.

TDS for NRIs on debt fund redemptions: The AMC deducts TDS at 30% plus cess on the gains — the maximum slab rate — since the gains are treated as regular income. If your actual tax liability is lower than 30%, the difference can be claimed as a refund by filing an ITR.

This is a significant change from the pre-2023 rules where debt funds held for three or more years qualified for LTCG at 20% with indexation. That benefit no longer exists for new investments.

For NRIs, this changes the relative attractiveness of debt mutual funds quite significantly. In many cases, an NRE fixed deposit — where the interest is completely tax-free in India — may deliver a better after-tax return than a debt mutual fund taxed at slab rates. If you’re not sure which option is more tax-efficient for your specific situation, our team can help you run the numbers.

Hybrid Mutual Funds: It Depends on the Equity Split

Hybrid funds invest in a mix of equity and debt. Their tax treatment depends entirely on how much equity the fund holds:

Equity ≥65% (aggressive hybrid, equity savings with high equity): Taxed exactly like equity funds. STCG at 20%, LTCG at 12.5% above ₹1.25 lakh. Holding period threshold: 12 months.

Equity between 35% and 65% (balanced hybrid, dynamic asset allocation): These get a middle-ground treatment. Holding period threshold for LTCG is 24 months. LTCG is taxed at 12.5%. STCG (units held under 24 months) is taxed at slab rates.

Equity below 35% (conservative hybrid): Taxed like debt funds. Gains at slab rates regardless of holding period for units bought after April 2023.

The visual alongside this blog maps out these rates across all three fund types in a single table — worth referencing as you read through.

What Makes NRI Taxation Different from Resident Investors

The tax rates on capital gains are the same for NRIs and resident Indians. But the mechanics are different in four important ways:

TDS is deducted automatically. Resident investors in equity funds don’t face TDS on redemption — they self-assess and pay tax when filing their ITR. NRIs have TDS deducted at source by the AMC on every redemption, at the applicable rates. This means your proceeds arrive after tax is already withheld.

The basic exemption limit doesn’t reduce your capital gains tax. Resident investors can use the basic exemption slab (₹2.5 lakh under old regime, ₹4 lakh under new) to offset capital gains if they have no other income. NRIs cannot do this. Your capital gains are taxed at the applicable rate regardless of whether your total Indian income falls below the basic exemption threshold.

Dividends are taxed at source too. Dividend income from mutual funds is taxed at slab rates for all investors. But for NRIs, the AMC deducts TDS at 20% plus applicable surcharge and cess on all dividend payouts. If your actual slab rate is lower, you claim the excess through an ITR.

You may be paying tax twice — unless you file correctly. If your country of residence also taxes your Indian mutual fund gains, you could end up paying tax in both India and abroad on the same income. India has DTAA treaties with over 90 countries to prevent this. But the benefit isn’t automatic — it requires specific documentation to be in place, including a Tax Residency Certificate from your country of residence and the relevant declarations filed with Indian tax authorities. Without these, the full Indian TDS rate applies and you lose the treaty benefit entirely.

DTAA paperwork is one of the most commonly missed steps among the NRI clients we work with. Getting it set up correctly — before you invest, not at tax filing time — is part of the onboarding process our team handles. If you’re not sure whether your documentation is in order, reach out and we’ll check.

The SIP Tax Nuance Every NRI Should Know

If you invest through a “systematic investment plan (SIP)“, each monthly installment is treated as a separate purchase for tax purposes. When you redeem, gains on each installment are calculated individually — some may be STCG (held under 12 months) and others LTCG (held over 12 months), even within the same redemption.

This creates a practical optimisation opportunity: by timing your redemptions so that as many installments as possible have crossed the 12-month mark, you shift gains from the 20% STCG bracket to the 12.5% LTCG bracket — and the first ₹1.25 lakh of LTCG in any financial year is exempt entirely.

For NRIs with large SIP portfolios, splitting redemptions across two financial years can also double the ₹1.25 lakh LTCG exemption — effectively making ₹2.50 lakh of gains tax-free instead of ₹1.25 lakh.

This is the kind of tax optimisation that makes a meaningful difference over time and is straightforward to execute with proper planning.

Filing Your ITR: Not Optional If You Want Your Money Back

TDS is not your final tax. It’s an advance collection by the government, often at rates higher than your actual liability. The only way to recover the excess is by filing an Indian income tax return.

NRIs must use ITR-2 for most mutual fund investment situations. The due date is 31 July of the following financial year (for FY 2025-26, that’s 31 July 2026).

Even if your total Indian income falls below the taxable threshold, filing is worth it if TDS has been deducted — because without filing, you forfeit the refund. You also lose the ability to carry forward capital losses, which can be set off against future gains for up to eight years.

Our team handles ITR filing for NRI clients as part of our ongoing service. If you’re unsure whether you have TDS refunds waiting to be claimed, a quick review of your investment statements usually reveals the answer within minutes. Get in touch and we’ll take a look.

The Key Numbers to Remember in 2026

For a quick reference on the current tax position:

Equity MF (≥65% equity): STCG 20% (held <12 months). LTCG 12.5% above ₹1.25L exemption (held ≥12 months). TDS: same rates.

Hybrid MF (35–65% equity): LTCG 12.5% after 24 months. STCG at slab rates. TDS varies.

Dividends: Slab rates. TDS for NRIs: 20% + surcharge + cess.

These rates apply as of FY 2025-26 and are subject to change in future budgets. If you want to understand exactly how these rates translate to your specific portfolio and country of residence, our team works through this with NRI clients regularly. Reach out for a personalised tax review — no obligations, just clarity on what you’re paying and whether there’s room to optimise.

Frequently Asked Questions

Disclaimer: This blog is for general informational purposes only and does not constitute tax or financial advice. All tax rates, thresholds, and rules reflect the position as of FY 2025-26 and are subject to change in future Union Budgets. Mutual fund investments are subject to market risks. NRIs should consult a qualified tax advisor for guidance specific to their country of residence and individual tax situation. DTAA benefits depend on specific treaty provisions and require proper documentation — consult a tax professional before relying on treaty relief. We specialise in Indian financial products and Indian tax laws; for tax obligations in your country of residence, please consult a local advisor.