Real estate is the default investment for most NRIs. Ask any Indian family living abroad where they want to put money in India, and property comes up almost every time. It’s familiar, it’s tangible, and it feels like a permanent connection to home.

We understand the appeal. But our job is to give you the full picture, not just the emotional case, but the financial one. And when you look at what real estate actually costs and returns for NRIs specifically, not for a resident Indian, but for someone managing property from abroad, the comparison with equity mutual funds looks quite different from what most people expect.

This blog lays out the honest numbers.

What FEMA Allows, and Doesn't Allow

Before the investment case, a quick word on what NRIs can actually buy. Under the “FEMA guidelines“, NRIs can purchase residential and commercial property in India without any limit on quantity or value, and without RBI approval. You can buy an apartment in Mumbai, an office space in Bangalore, or a villa in Goa. No restrictions on how many.

What you cannot purchase is agricultural land, plantation property, or a farmhouse. This prohibition is strict, the penalties for violation can be as high as three times the transaction value. It applies regardless of how a seller describes the land, so RERA verification and clear title confirmation are essential before any property transaction.

For most NRI investors focused on residential or commercial property, the restriction isn’t the issue. The issue is whether the investment itself stacks up.

The Cost That Starts Before You've Invested a Rupee

Every property purchase in India carries an entry cost that most investment comparisons conveniently leave out: stamp duty and registration charges.

Stamp duty rates across major Indian cities currently sit between 5% and 7% of the property value, with Mumbai at 6%, Pune at 7%, Delhi at 6% for male buyers, and Bangalore at 5% for properties above ₹45 lakh. Registration adds roughly 1% on top. In total, an NRI buying property in a major city is typically paying 6–8% of the property value before the investment even begins.

On a ₹50 lakh property, that’s ₹3–4 lakh in upfront costs that earn you nothing and are not recoverable. On a ₹1 crore property, you’re looking at ₹6–8 lakh gone before you’ve collected a single rupee of rental income or seen a single rupee of appreciation.

There is no equivalent entry cost in mutual funds. You invest ₹50 lakh, you own ₹50 lakh of units from day one.

This entry cost matters enormously for long-term return calculations. A 7% annual appreciation on a property purchased for ₹50 lakh actually needs to be calculated against your total outlay of ₹53–54 lakh, reducing the effective annualised return from day one.

The Rental Reality for NRI Landlords

Many NRIs buy property expecting steady rental income. The gross rental yield on residential property in most Indian cities sits between 2% and 4% annually. On a ₹50 lakh property, that’s ₹1–2 lakh per year before any deductions.

What most people don’t factor in is the tax treatment of rental income for NRIs. Your tenant is required to deduct TDS at 31.2% on your rent, from the first rupee, with no minimum threshold that applies to resident landlords. There’s no exemption for small rents. If your tenant doesn’t comply, the liability ultimately falls back on you as the property owner.

After the 31.2% TDS deduction, your net rental income drops significantly. You can file an ITR to claim a refund if your actual tax liability is lower, but that requires annual India-side filing and coordination.

Beyond tax, there are the operating costs: property tax, society maintenance charges, repairs, and the inevitable periods of vacancy when a tenant leaves. On a realistically managed residential property, net rental yields after all deductions and costs for NRIs typically land at 1.5–2.5% per annum, not the 3–4% the gross figure suggests.

If managing tenants and maintenance from Dubai, London, or Toronto sounds straightforward, consider what it actually means in practice: finding reliable tenants remotely, coordinating repairs without being there, dealing with rent defaults from thousands of miles away. Most NRI landlords either rely on a trusted family member in India (not always available or reliable) or a property management service that charges 8–12% of annual rent.

This is one of the friction points we see most often with NRI clients who already own property. If you’re evaluating whether to add more real estate or redirect capital to a managed investment structure, a conversation with our team can help you think through the real net return on what you already own, before committing to more.

Selling Property as an NRI: Where It Gets Complex

The exit from Indian property is where NRI investors face their most significant friction, and where most articles fall short on detail.

When an NRI sells property, the buyer is legally required to deduct TDS from the sale proceeds before transferring any money. For long-term capital gains (property held for more than two years), this TDS is currently deducted at 20% of the full sale consideration, not 20% of the gain, but 20% of the entire sale price. On a ₹1 crore sale, that’s ₹20 lakh withheld immediately.

The actual long-term capital gains tax owed is 12.5% on the profit (without indexation for properties acquired after July 23, 2024). So on a ₹30 lakh gain, your real tax liability is ₹3.75 lakh, but the buyer has already withheld ₹20 lakh. You file an ITR, claim the refund, and eventually recover the difference. But “eventually” can take one to two financial years, during which your capital is locked.

The Budget 2026 has simplified the buyer-side compliance by removing the TAN requirement from October 2026, but the substantive TDS deduction rates and the NRI seller’s obligations remain unchanged.

Then come the repatriation rules. Your sale proceeds land in your NRO account in India first. Repatriation from NRO is capped at USD 1 million per financial year, roughly ₹8.78 crore at current rates. For most NRI property sales this won’t be a constraint, but for higher-value properties or multiple transactions in a single year, planning across financial years becomes necessary.

Compare this to redeeming mutual fund units: proceeds settle within two to three business days, are credited to your linked NRE or NRO account, and repatriated freely if invested via NRE.

If you’re planning a property sale and want to understand the tax timing, repatriation sequencing, and what to do with the proceeds, our team regularly helps NRI clients navigate exactly this transition.

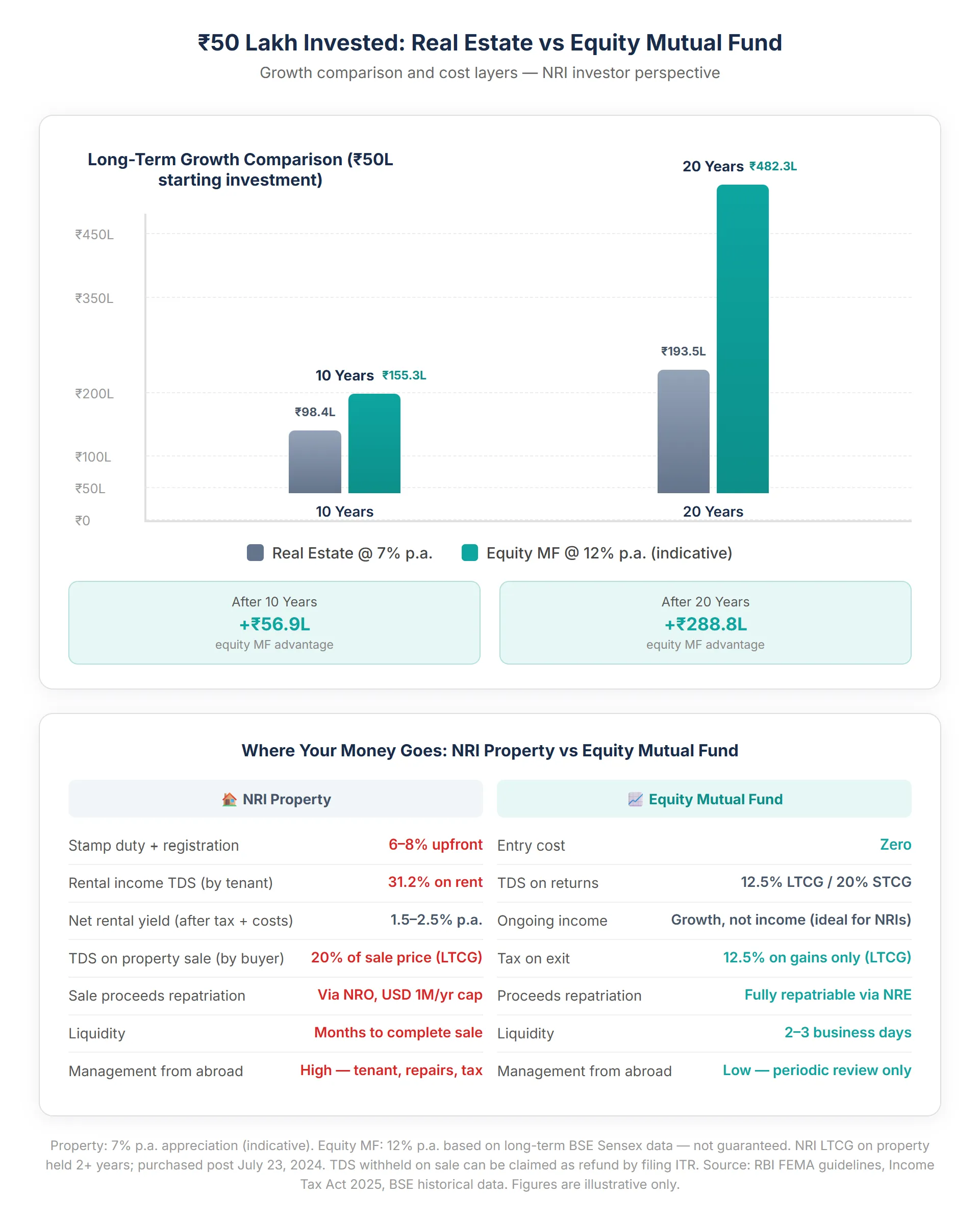

What the Growth Numbers Look Like

Here’s what ₹50 lakh invested in each option looks like over 10 and 20 years, under reasonable assumptions,7% annual appreciation for residential property (a generous figure for most Indian cities), and 12% for equity mutual funds based on long-term BSE Sensex historical returns:

These numbers do not yet account for the entry cost disadvantage (6–8% stamp duty reduces your real starting capital for property), the rental income advantage (property generates 1.5–2.5% net annually), or the exit TDS friction. When you factor all of those in, the long-term equity advantage typically widens, not narrows.

The visual alongside this blog shows the growth trajectory across both options, and the key cost layers that the headline figures miss.

Important: Property appreciation at 7% is an assumption for illustrative purposes and varies significantly by city, locality, and time period. Equity MF returns at 12% are based on long-term BSE Sensex historical data and are not guaranteed. Both figures are indicative only. Mutual fund investments are subject to market risks.

When Real Estate Does Make Sense for NRIs

This isn’t an argument against property ownership. There are clear situations where real estate makes genuine sense for NRIs.

A home for your return. If you have a clear plan to return to India within five to seven years, owning a property you’ll actually live in is different from owning it as a pure investment. You avoid future rental costs, and the emotional value of having your home ready is real. Just don’t confuse “home I plan to live in” with “investment generating financial returns.”

Commercial property with higher yields. Commercial property, well-located office space, retail units, or warehouses, can generate gross rental yields of 6–9% annually, meaningfully higher than residential. The operational complexity is similar, but the income case is stronger. This segment requires careful due diligence on tenant quality and RERA compliance.

Inherited property. If you’ve inherited property in India, the calculus is different, you didn’t pay the stamp duty, and the question is whether to hold or sell and redeploy into liquid assets. We’d be happy to help you think through that specific situation.

Anchor asset for family. Some NRIs maintain property in India specifically as accommodation for ageing parents or as a family base during annual visits. This is a legitimate use of capital, just categorise it as a lifestyle asset, not an investment, and structure the rest of your portfolio accordingly.

The Framework for Deciding

Before committing capital to Indian property, we’d encourage any NRI to honestly answer four questions:

- Can I manage this from abroad? Not theoretically, practically. Do you have a trusted person in India who can handle tenants, repairs, and annual inspections? Or are you planning to hire a property management service and absorb that cost?

- Have I factored in the real entry cost? Stamp duty, registration, and any brokerage on purchase typically add 8–10% to your total outlay. Your investment needs to appreciate past that before you’ve made a rupee.

- Do I understand the exit? TDS on the sale, repatriation through NRO, and a potential one-to-two year refund cycle are standard for NRI property sellers. Is your capital available for that timeline?

- Is this the right use of this capital given my goals? If the money is meant to grow over 15–20 years, the long-term numbers strongly favour equity. If it’s for a specific purpose like a return home or family accommodation, the equation is different.

We work through exactly this framework with NRI clients who are deciding between property and financial investments. For those already holding property, we help assess whether the capital is working hard enough, or whether a reallocation makes sense. If you’d like to have that conversation, reach out to our team. There’s no commitment, just a clear, structured look at your situation.

Frequently Asked Questions

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. The return assumptions used in this blog (7% for property appreciation, 12% for equity mutual funds) are illustrative estimates based on historical data, they are not guaranteed and actual returns will vary. Property appreciation rates differ significantly by city, locality, and time period. TDS rates, stamp duty charges, and tax regulations are subject to change, always verify the current position with a qualified tax advisor and legal professional before any property transaction. This blog is for general informational purposes only and does not constitute financial, legal, or tax advice. NRIs should consult a qualified advisor for guidance specific to their country of residence and individual circumstances. We specialise in Indian financial products and Indian tax laws only.